Here is a summary of real GDP Growth projected for the year 2022 (and previous year) by IMF.

UK: 3.6 (7.4) EU: 3.1 (5.2) Germany: 1.5 (2.6) France: 2.5 (6.8) Italy: 3.2 (6.7) Spain: 4.3 (5.1)2022年11月2日水曜日

2022年11月1日火曜日

For the third quarter, analysts expect annualized gains of 3.2%

https://www.japantimes.co.jp/news/2022/08/15/business/economy-business/japan-economy-recovery/

The Japanese economy — the world’s third largest — recovered to its pre-pandemic size in the second quarter, as consumer spending picked up following the end of coronavirus curbs on businesses.

Gross domestic product grew at an annualized pace of 2.2% in the second quarter of 2022, coming in below the median estimate of 2.6%, Cabinet Office data showed Monday. That lifted the size of the economy to ¥542.1 trillion ($4.1 trillion), above what it was at the end of 2019. First-quarter GDP was revised to an expansion from a prior contraction.

"The economy managed to return to its pre-pandemic size, but its recovery pace has been slower than other nations,” said economist Takeshi Minami at Norinchukin Research Institute. "I expect growth to continue in the third quarter too, but it will likely be losing momentum down the road.”

The end of pandemic restrictions on businesses in late March helped spur the economy. Consumer spending, which accounts for more than half of Japan’s economic output, led the growth, as did capital expenditure. The relaxing of COVID-19 rules resulted in increased spending at restaurants and hotels, as well as on clothes, according to the Cabinet Office.

Still, the gains were more limited than expected a few months ago, showing that pent-up demand among consumers has been moderate.

While the economy regained its pre-pandemic size, economists expect the central bank to stick to its current easing policy and the government to continue providing support for households hit by both the pandemic and rising prices. In contrast, other developed economies are doing the opposite by raising interest rates to cool demand and rampant inflation.

Japan’s milestone also comes behind the U.S.’s, which recovered its pre-pandemic economy size a year ago, while much of Europe regained it at the end of 2021.

The report came out as downside risks mount at home and abroad. Japan has been reporting record COVID-19 infection cases with daily numbers continuing to top 200,000 this month. The government has so far kept economic activity as normal as possible without bringing back restrictions. But high-frequency data suggest people’s mobility is falling.

In Japan’s key trading partners, growth is slowing as the U.S. and Europe fight inflation and China sticks to its "COVID zero" policy. The war in Ukraine continues to disrupt food and energy supplies while the crisis in Taiwan is adding to geopolitical risks.

Inflation remains relatively moderate in Japan, but consumption may cool with prices rising faster than wages. After factoring in inflation, paychecks in Japan have been falling for three months in a row through June.

Prime Minister Fumio Kishida ordered another set of measures Monday to contain inflation by early September, with a boost in funding for regional governments and a continued cap on imported wheat prices. He emphasized that wage gains need to be sustained, while saying that the additional support measures will concentrate on food, regional grants and energy.

For now, the measures will be supported by existing reserve funds, though Kishida said he’ll remain flexible in his approach.

"Inflation can cool consumption, although oil prices may stabilize with the global economy slowing down,” said Norinchukin’s Minami. "As downside risks mount in the world economy, there’s a risk that Japan’s economy could contract at some stage toward the end of the year.”

So far, economists expect growth in Japan to remain moderate for the rest of the year, slowing as the months progress. For the third quarter, analysts expect annualized gains of 3.2%.

6.7兆円規模の介入だと26回介入できる計算。毎月1回介入しても2年間以上続けられる

1.2兆ドルの外貨資産をいまの為替レート(1ドル148円)で日本円に換算すると177兆円ぐらい。6.7兆円規模の介入だと26回介入できる計算。毎月1回介入しても2年間以上続けられる。

そのうえ、使用した外貨資産はどぶに捨てる(資産が減少している)わけではなく、売ってその対価を受け取っているわけで、一つの資産(ドル)が別の資産(円)に移動したに過ぎない。つまりいつでもまた外貨資産に換えることができる。 たとえ円安傾向の中であってさえも、実際の為替は小さな上下変動を繰り返しながら円安方向に動くので、その小さな変動を利用して、円をドルに換えても資産を増やすことは可能です。つまり為替介入は理論的には永遠にできる。 しかも、現在保有する外貨資産1.2兆ドルが、ドル安時代の1ドル100円で買われたものと仮定すると、120兆円だったその外貨資産は、ドル高為替変動で177兆円に膨らみ、ドル高変動で57兆円の増益を生じている。日本の一般会計総予算は110兆円なので、その半分以上に値する収益です。Japanese Halloween is in fact nothing but a festival for cosplayers

Japanese Halloween is a kind of Wakon-Yosai (和魂洋才), adopting a Western culture but in uniquely Japanese way. It's like breathing a Japanese life into a Western body, so to speak.

Before Halloween became popular in Japan, there was a such thing in Japan called Cosplay (コスプレ), or Costume Play, "an activity and performance art in which participants called cosplayers wear costumes and fashion accessories to represent a specific character". (Wikipedia)

Here is a sample of cosplay by the current Tokyo Governor, Yuriko Koike, for a Halloween party a few years ago:

https://www.sankei.com/photo/story/news/161029/sty1610290008-n1.html

Japanese Halloween is in fact nothing but a festival for cosplayers, without reference to stories behind Halloween, a peculiar Japanese practice in which its meaning is dropped and only its form is adopted.

You can see this practice, for example, in some Japanese weddings that are performed in Christian forms, but without any Christian faith.

Now, Japan has a long history of cosplay in traditional performing arts:

Kabuki - https://en.wikipedia.org/wiki/Kabuki

Kagura - https://en.wikipedia.org/wiki/Kagura

Noh - https://en.wikipedia.org/wiki/Noh

etc.

2022年10月31日月曜日

ハロウィンがコスプレの祝日(言い訳)になった

コスプレはもともと日本の文化であって、たまたま表面上ハロウィンがそれに似ているので、ハロウィンがコスプレの祝日(言い訳)になった、とぼくは理解している。もう日本のお祭りの一つになったと言っていいと思うよ。

物価3%で円安も150円台、日銀が動かない理由は?

https://www.nikkei.com/article/DGXZQOUB284SV0Y2A021C2000000/?unlock=1

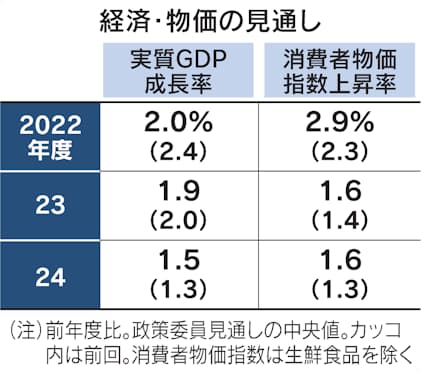

日銀は27~28日の金融政策決定会合で大規模緩和の現状維持を決めました。9月の消費者物価指数(CPI、生鮮食品除く)は前年同月比で3.0%の上昇率となり、日銀が目標とする2%を大きく上回りました。悲願の2%を達成したのに日銀が動かないのは「物価上昇は一時的」とみているからです。

実際、日銀が決定会合後に公表した「経済・物価情勢の展望(展望リポート)」からは、2023年度のインフレ率を1.6%とみていることがわかります。日本経済研究センターの調査でも、民間エコノミスト36人の予測は同1.25%で、足元の物価上昇は「原油価格の高騰による一時的なもの」との見方が現時点では大勢のようです。

日銀が利上げに転じれば、住宅ローン金利も上がって家計には重荷となります。中小企業は新型コロナウイルス危機下で積み増した借金を抱えたままです。政府財政も利払い負担が重くなるでしょう。日銀の利上げだけで世界的な原油高やドル高を抑えられるわけではなく、じっと動かない日銀の判断にも合理性はあります。

本心は「最後の好機」とみている?

もっとも多くの日銀関係者に聞いてみると、動かない理由はもう少し深いようです。「黒田日銀は足元の物価高を、長年のゼロインフレから脱するラストチャンスとみている」との指摘が多く上がりました。どういう意味なのでしょうか。

歴史を振り返ると日本のインフレ率は、1990年代後半からほぼゼロで止まってしまいました。銀行危機が深刻だった98年を起点とすると、2021年までの20年強でCPIはわずか1.1%しか上昇していません。1998年までの20年間で1.5倍も上昇したのと対照的です。

これだけ長くゼロインフレが続くと、生活者心理として物価が上がらないのが当たり前になってきます。米欧では交通運賃や公共料金ですら頻繁に上がりますが、ゼロインフレが当たり前の日本では大騒ぎになるので、簡単に値上げできなくなります。日銀はこれを「ゼロインフレのノルム(社会通念)」と言っています。

一方で足元のインフレが長く続けば、このノルムを吹き飛ばす材料になる可能性があります。食品などの相次ぐ値上げで、今では生活者の多くは「ゼロインフレが当たり前」とは少しずつ思わなくなってきました。円安は外国人旅行客を呼び込んで宿泊や飲食のニーズを増やす効果もあり、サービス産業の賃上げに直結するかもしれません。日銀は金融緩和を維持することで、こうした好循環を期待しているようです。

物価高と円安を日銀が放置することにはリスクもあります。円安の一因は日銀の緩和維持による日米金利差にあります。円安が一段と進んで企業や生活者のコスト高が強まれば、2%インフレが定着する前に日本経済が減速してしまう懸念が出てきます。ゼロインフレのノルムを吹き飛ばすという発想は、一種の賭けと言えるかもしれません。

日銀が引きずる過去のトラウマ

日銀が動かない理由として、もう少し後ろ向きな話も漏れてきます。それは過去のトラウマです。日銀は黒田総裁が就任する前、デフレを引き起こしたとして政界から厳しく批判されました。そのやり玉に挙がったのが、2000年のゼロ金利解除と、06年の量的緩和解除です。いずれも解除後に結果的には再びインフレ率がマイナス圏に戻ってしまい「拙速な緩和縮小」と指弾の材料になりました。

足元でみても、世界経済は米欧の急激な金融引き締めで23年にも景気後退に突入するリスクがあります。世界的な景気悪化が起きれば日本経済も影響は避けられず、そんな間際に日銀が緩和縮小に転じれば「拙速な引き締め」と非難されるのは必至でしょう。トラウマからくる組織防衛の意識も、日銀の判断を縛る材料になっているようです。

もっとも、世界的な景気悪化が発生すれば次なる問題が持ち上がります。米欧は金融引き締めから再び金融緩和に転じるでしょう。米連邦準備理事会(FRB)も欧州中央銀行(ECB)も22年の大幅利上げで、次なる危機に備える利下げ余地を獲得しました。一方の日銀は利下げ余地がないままで、次なる景気悪化の影響を和らげる力がありません。外国為替相場も今度は大幅な円高になる可能性があります。

景気が安定すれば金利を緩やかに引き上げておき、景気悪化時に果敢に利下げに転じる。金融政策とは本来、こうした柔軟性と機動性が最大の武器だったはずです。「動かない日銀」の大きな問題は、次なる景気悪化に備える余力を持てないことにありそうです。

(金融部長 河浪武史)

「為替介入は広く行われており、政策ツールとして有効である。成功率はおよそ80%にも上る」

https://www.aeaweb.org/articles?id=10.1257/mac.20150317

『アメリカンエコノミックジャーナル:マクロ経済』誌の2019年号に発表された論文「為替介入はどんな時に有効かー33か国からのエビデンス」という論文では、「為替介入は広く行われており、政策ツールとして有効である。成功率はおよそ80%にも上る」と結論しています。

ここで「成功」と言っているのは「為替レートの変動を鎮静化(stabilize)させること」です。財務省や日銀が為替介入の理由について必ず発言していることは「急激な変動」への対応ですが、雑誌の「鎮静化(stabilize)」とほぼ同じ意味だと言えます。日銀の黒田総裁も「円安が穏やかであれば、円安は日本経済にとってプラス」と繰り返し述べています。 つまり、論文の主旨は、為替介入の目的が、変動(円高傾向や円安傾向)をストップさせたり逆方向へ転換させたりすることではなく、急激な変化をゆるやかにすることを目指している場合、その成功率はかなり高い、ということですが、日本の為替介入目的もまさにそれに合致するわけです。 ところで、今回の日本の為替介入は、その意味で、いまのところ成功していると言っていいと思います。大型介入直前9月21日では1ドルあたり144.31円でしたが、現在(10月30日)は147.45円です。この40日間に3.14円(2.1%)安になっています。介入前の40日間の変動はというと、8月10日では1ドルあたり132.83円でしたが、それが40日後には144.31円になっています。その40日間では11.84円(8.6%)安になっています。つまり、介入後の円安幅は介入前と比べて、11.84円(8.6%)から3.14円(2.1%)へと、かなり抑えられている結果(ほぼ4分の1)となっています。

登録:

投稿 (Atom)

日米共同声明に抗議 日本公使に「強烈な不満」表明―中国

https://www.jiji.com/jc/article?k=2025021000786&g=int 日米共同声明に抗議 日本公使に「強烈な不満」表明―中国 時事通信 外信部 2025年02月10日19時18分 配信 中国外務省=北京(AFP時事) 【北京時事】...

-

Unknown: 44.8% China 11.9% Russia 11.6% Iran 5.3% N Korea 4.7% Ukraine 2.6% USA 2.3% Pakstan 1.8% Turkey 1.7% Other countries 13.4% https:/...

-

https://www.reuters.com/article/factcheck-pfizer-vaccine-transmission-idUSL1N31F20E In the video, Roos then introduces the testimony clip s...

-

Basically, this video shows that the Ainu and Japanese share common DNA from the ancient Jomon people, the oldest known inhabitants of the...